- English

- 简体中文

- Afrikaans

- שפה עברית

- icelandic

- Hrvatski

- Монгол хэл

- Lëtzebuergesch

- Español

- Português

- русский

- Français

- 日本語

- Deutsch

- tiếng Việt

- Italiano

- Nederlands

- ภาษาไทย

- Polski

- 한국어

- Svenska

- magyar

- Malay

- Dansk

- Suomi

- Türkçe

- العربية

- Indonesia

- Norsk

- český

- ελληνικά

- فارسی

- български

- Latine

- Slovenský jazyk

- Slovenski

- Srpski језик

- বাংলা ভাষার

- हिन्दी

- Pilipino

- Gaeilge

- تمل

- український

- Javanese

- தமிழ்

- नेपाली

- Burmese

- ລາວ

- Қазақша

- Azərbaycan

The Eye-catching Q4 Performance of Global Semiconductor Market in 2023

According to data from the World Semiconductor Trade Statistics (WSTS), the global semiconductor market saw a quarter-over-quarter increase of 8.4% in Q4 of 2023. This 8.4% growth has hit the peak since the 9.1% in the second quarter of 2021 which marks the highest growth from the third to the fourth quarter in the past 20 years!

Main driving force in Q4 Memory chips

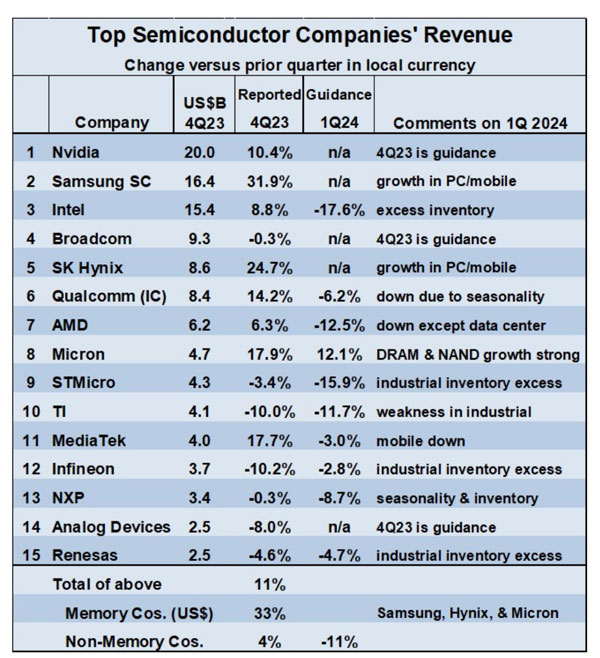

This strong growth was mainly driven by memory chips. Memory companies all reported healthy revenue growth in Q4 of 2023 compared to Q3.

Measured in dollars, Samsung’s memory business grew by 49%, SK Hynix by 24.1%, and Micron Technology by 17.9%. The weighted average revenue growth rate of these three companies, was 33% calculated in dollars. In comparison, the weighted average dollar-denominated revenue growth rate for the twelve largest non-memory companies from Q3 to Q4 of 2023 was 4%.

The non-memory company with the largest growth was MediaTek, with an increase of 17.7%, followed by Qualcomm with 14.2%, and Nvidia with 10.4%. Among them, seven non-memory companies experienced revenue declines in Q4 of 2023, with Infineon dropping by 10.2%, Texas Instruments by 10.0%, and ADI by 8.0%.

Apart from memory companies, the revenue outlook for the next quarter for other semiconductor companies is mostly negative.

Micron is expecting a growth of 12.1%. Samsung and SK Hynix did not provide specific guidance but both indicated that memory demand remains strong. Meanwhile, nine non-memory companies are projecting drops ranging from 2.8% for Infineon to 17.6% for Intel in the first quarter of 2024. The anticipated declines are attributed to seasonality, excess inventory, and weakness in the industrial sector.

How will smartphones, PCs, automobiles, and the industrial sector impact semiconductor companies in 2024?

What developments can be expected in 2024 for a range of applications driving the semiconductor market?

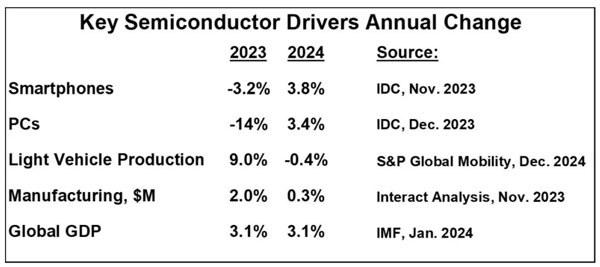

Smartphone shipments declined by 3.2% in 2023, but IDC expects them to rebound in 2024 with a growth of 3.8%. Smartphones have driven revenue growth for memory companies, Qualcomm, and MediaTek.

Personal computer (PC) shipments experienced a sharp decline of 14% in 2023. IDC predicts that PCs will grow by 3.4% in 2024. The rebound in PCs will benefit memory companies and processor companies such as Intel, Nvidia, and AMD.

What developments can be expected in 2024 for a range of applications driving the semiconductor market?

Smartphone shipments declined by 3.2% in 2023, but IDC expects them to rebound in 2024 with a growth of 3.8%. Smartphones have driven revenue growth for memory companies, Qualcomm, and MediaTek.

Personal computer (PC) shipments experienced a sharp decline of 14% in 2023. IDC predicts that PCs will grow by 3.4% in 2024. The rebound in PCs will benefit memory companies and processor companies such as Intel, Nvidia, and AMD.

The automotive and industrial markets have become major revenue drivers for some companies, due to the weakness in other end markets. However, 2024 appears to be the end point for growth in auto production.

According to S&P Global Mobility forecasts, light vehicle production is expected to decline by 0.4% in 2024, after a strong growth of 9% in 2023. S&P states that vehicle production and inventory replenishment have met recent demand and even exceeded current customer requirements. Based on data from Interact Analysis, global manufacturing (industrial production) is projected to slow from a growth of 2.0% in 2023 to 0.3% in 2024. This indicates a slowdown in industrial sector demand. The deceleration in the automotive and industrial sectors primarily impacts semiconductor companies such as STMicroelectronics, Texas Instruments, Infineon Technologies, NXP Semiconductors, Analog Devices Inc. , and Renesas Electronics.

The growth of the semiconductor market in 2024 will be driven by memory.

WSTS predicts that memory will grow by 44.8%, and non-memory will grow by 6.5%, thus driving the total market to a 13.1% increase in 2024. Gartner, in its forecast, assumes a memory growth of 66%, with the overall market growing by 16.8%. Memory will be driven by a recovery in the personal computer and smartphone markets. These two areas will also aid the non-memory market, but other non-memory markets like automotive and industrial are expected to be weaker drivers in 2024.

Against this backdrop, what is the outlook for the overall semiconductor market in 2024? Most forecasters expect robust growth, with IDC’s highest projection being “over 20%.” Objective Analysis forecasts growth at “under 5%,” as they believe the memory boom is unsustainable. Semiconductor Intelligence’s latest forecast shows an 18% growth. Other forecasts range between 10.5% and 17%.

Source:Wechat public account under ICHUNT.COM Feb.21st.2024 PM12:03 Canton China

Note: This article synthesizes information from WSTS, among others. The cover image/illustrations are sourced from the internet, and the copyright of the images belongs to the original authors. This article is for reference, learning, and communication purposes only, and does not constitute any advice or represent the stance of our company. If there are any issues, please do not hesitate to contact us.